A couple of years ago I was contacted by a local bank that was trying to put together a 7a working capital loan for one of their clients. The client was running a fast growing service business but was having some severe cash flow issues that were beginning to jeopardize the entire enterprise. This company was growing quickly through acquisition of large, stable, long-term customers. The problems was that as the company’s income was increasing, their cash position was becoming critical. Basically the client was growing so fast that they were going broke.

The lender asked me to work with the customer to create a comprehensive 3 year financial model so that they had a very clear picture of exactly how much additional working capital would be required to sustain the company. The graveyard of small business has an entire section stuffed full of companies that had great potential but ultimately failed due to cash flow issues. The company had a very close relationship with their bank and the bank wanted to assure their long term success. They felt that their customer needed a large working capital line of credit to smooth out their cash flow issues and wanted a detailed cash flow analysis to assure that they were providing a large enough line of credit to sustain the company through their growth stage and into the long term.

In simple terms here was the situation – common to many service businesses, The company created a new service and signed a contract to do work for a new customer. This work is on-going and will be monthly, and paid Net 30.

Let’s make this a bit more personal. You are the owner of VendorCo and your customers are CustomerCo.

VendorCo is a stable company that is profitable but not cash-rich.

CustomerCo (1, 2 and 3) are large enterprises that need to outsource certain functions to third parties. This could be IT functions, security, janitorial or maintenance services, etc. CustomerCo has an excellent D&B rating and plenty of cash. Prospect of payment is not an issue.

As an ongoing contract, the income looks like this:

CustomerCo-1 agrees to pay $25,000/4wks for specific services to be performed by VendorCo. VendorCo employees who perform this service have a total cost of $22,000/4wks including all administrative overhead. End result is an additional $3,000/4wks of net income, Wohoo!

VendorCo has begun to develop a reputation for excellence in the industry and because of this they are adding an average of one new customer a month over 3 months. Sounds great, doesn’t it. But this growth has put them on the road to disaster.

How are they going broke? This is all great news and should lead to an additional $9,000/4wks of net income – $117,000/52wks on the PLUS side!

Not Yours.

That is BMW M6 Gran Coupe money! But instead of driving around in your new 560hp twin-turbo V8 Bavarian luxury car, you are fending off bill collectors and looking at an overdrawn bank account.

WHAT IN THE WORLD HAPPENED?

Income is great, the problem is Cash Flow. Let’s take a look:

Start with a four assumption:

1) VendorCo has $30,000 in cash on hand.

2) VendorCo has current monthly net operating income from continuing operations of $10,000/4wks – This income is used to pay your salary, meaning the company is currently at break-even when you include the owner’s draw.

3) CustomerCo is billed at the end of each month for work performed, All invoices are Net -30 – Payment is deposited on day 1 of following month.

4) Employees are paid every two weeks (for simplicity) for the previous period. Work weeks 1 and 2. Cash Outflow for paycheck is in Week 3.

So, what happens when VendorCo signs a new customer?

1) VendorCo signs a contract to provide services to a large organization (CustomerCo-1).

2) VendorCo hires/purchases/trains additional resources to support new customer.

3) VendorCo begins working for CustomerCo-1.

5) VendorCo must pay employees who worked on new contract.

6) VendorCo bills CustomerCo-1, Net 30.

7) VendorCo must pay employees who worked on new contract.

8) Payment deposited 31 days after billing.

9) Go to step 3 and repeat for duration of contract.

So, for a single customer over a mythical 52 week year:

Revenue: $325,000

Expenses: $286,000

NET INCOME: $39,000

Do that 3 times and you are looking at (3 x $39,000) $117,000 NET INCOME over 52 weeks. So, where is my M6?

Your customers and employees have it.

The reality of this simple business model is that each customer will cost you $33,000 in cash during the first two months of service. According to your accounting statements you have made $6,000 in net income from this customer over the last 8 weeks, that is a difference of $39,000 THE WRONG WAY!

It gets worse…

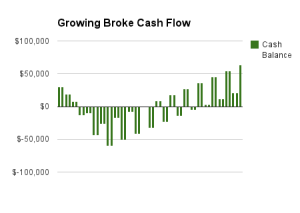

You will not be consistently cash flow positive on each customer until week 49 of your contracts.

So, add 1 new customer a month for 3 months and your maximum draw down is $90,000 in weeks 15 and 16. You started with $30,000 in cash but now you are overdrawn by $60,000.

NEGATIVE SIXTY THOUSAND DOLLARS.

WHAT!? HOW?! WHY?! But M6!!

Can You Survive Additional Customers?

Because you are financing your customer’s use of your employees for 45 days (3 pay periods).

This is where working capital comes into play. Working capital is defined as your current assets minus current liabilities. It is a measure of your ability to cover existing and up coming expenses.

If you are short working capital, you can not pay your bills.

If you can not pay your bills you go out of business.

Done, end of story. Polish off that resume because even though you had a profitable business you are back on the street in your freshly polished interview shoes, not in your freshly polished M6 Gran Coupe.

But this does not have to happen to you. You have heard the phrase “It takes money to make money” and that means working capital. All businesses need working capital and lack of adequate working capital is one of the primary reasons that an otherwise successful business goes under. The SBA 7(a) Loan program is one of many option you may have to assure your company success. Among other things like purchasing Real Estate, machinery or inventory, an SBA 7(a) loan can be used or provide long term working capital and really that is all you need to be a success: enough working capital to grow.

CONTACT A LENDER OR ASK FOR HELP

Sit down and take a good look at your business cash flow, or hire a professional to help you. Get a grasp of all of your income and expenses, your growth opportunities, and the cost of each of those opportunities. Keep in mind the gap that probably exists between when have to outlay cash (inventory, research and development, employees) and when you realize income from that expense. Using an Excel spreadsheet, you can even build a model to mirror your business cash flow and track your business against your projections. You can use the linked Google spreadsheets as a simple model on which to build. They are for an extremely simple business model but will provide you with the basic concepts you need to understand your fiscal situation.

Simple Google Spreadsheet Here: Growing Broke Cashflow Worksheet on Google

Understanding your cash flow is a critical part of understanding your business and it is not very difficult to build a rough map of your ongoing cash situation. If you find that you need additional working capital, take a look at the SBA 7(a) program.

After He Got a 7(a) loan

In the scenario above, you would need to have around $100,000 in working capital to survive your new customers. But once you are over the hump, your business cash flows like a champ. By the end of year 2 you will be able to pay back your $100,000 loan, have $100,000 in the bank and still have your company throw off an additional $9,000 in cash every 4 weeks.

If cash flow is causing you problems or your cash position is preventing you from growing, look into the SBA 7(a) program. It could allow you to build your business to its potential.